Conclusions

The goal of this research project was to examine how changes in U.S. economic and financial conditions transmit to South Korea’s financial markets and real economy. Using time-series methods on exchange rates,yield curve, equity indices, trade flows and housing data, the project aims to measure transmission and to show what these dynamics mean for real people in Korea in both macro and microecnomical ways.

To approach this goal, the analysis began with univariate ARIMA/SARIMA models as a baseline for each major series—policy rates, yield spreads, the KRW/USD exchange rate, trade, housing prices, and equity indices. These models highlighted several common features of the data: strong persistence, clear seasonality in trade and housing, and heavy-tailed behavior and occasional outliers in financial variables. Residual diagnostics often showed that simple ARIMA specifications captured broad trends and cycles reasonably well, but struggled with some short-run dynamics and volatility bursts, especially in trade and exchange-rate series. This step matters for real life because it shows that many key prices and quantities in Korea—interest rates, house prices, exports—do not quickly revert after a shock; instead, they tend to drift and adjust slowly, implying that adverse movements in funding costs or trade volumes can linger for households and firms rather than disappearing in a few months.

The multivariate ARIMAX/SARIMAX and VAR models then made the transmission channels from the U.S. to Korea much more explicit. In the equity VAR, U.S. stock performance, global risk sentiment (VIX), and U.S. yield spreads were modeled jointly with the KOSPI, revealing that U.S. conditions and global risk factors feed into Korean equities more strongly than the reverse and that tighter U.S. financial conditions tend to coincide with weaker Korean equity outcomes. For long-term rates and the Seoul housing market, the VAR showed that housing prices are largely driven by their own past values but are nonetheless shaped over time by U.S. and Korean 10-year yields, consistent with an affordability channel in which lower long rates gradually support property prices. SARIMAX models for the KRW/USD rate and for Korea’s exports to the U.S. pointed to interest-rate differentials, the broad dollar cycle, U.S. manufacturing activity, and risk proxies such as the VIX as central drivers; forecasts generally implied modest KRW appreciation when rate gaps narrow and risk cools, and a gentle upward trajectory for exports when U.S. demand is firm, with substantial month-to-month noise. For real people, this means that periods of rising U.S. rates and falling U.S. equities tend to be accompanied by a weaker KOSPI, tighter financing conditions, and more fragile export revenue, even if domestic fundamentals in Korea have not changed much.

Financial time-series models (ARCH/GARCH) were more focusing on volatility. Both KOSPI returns and KRW/USD returns displayed strong volatility clustering and clear ARCH effects: stable periods with small daily moves are interrupted by crisis windows, such as the global financial crisis, during which shocks are large and volatility remains elevated for an extended time. GARCH(1,1) specifications captured this persistence in conditional variance, implying that once uncertainty spikes in global markets, risk in Korean equity and FX markets does not immediately subside. In practical terms, this matters for Korean households who may face sudden swings in the cost of imported goods, foreign travel when the won becomes volatile, and for firms whose trade cost( as South Korea is a export-based country)become more fragile when FX and stock-market volatility stay high well after a global shock has hit.

The deep-learning section tested whether more flexible nonlinear models—RNNs, LSTMs, and GRUs—could improve forecasts for the U.S.–Korea yield spreads and Korean exports to the U.S. Compared with traditional ARIMA and SARIMAX benchmarks, the recurrent networks were able to learn complex temporal patterns but did not consistently outperform the best linear models in terms of RMSE, especially in the multivariate export setting. In fact, for exports, SARIMAX achieved the lowest test error while preserving a transparent link between U.S. demand, the exchange rate, and trade outcomes, with GRU models coming closest among the neural architectures but still at higher complexity and lower interpretability. This comparison suggests that, for macro-financial data of this type, well-specified linear time-series models remain powerful tools for policy and risk analysis.

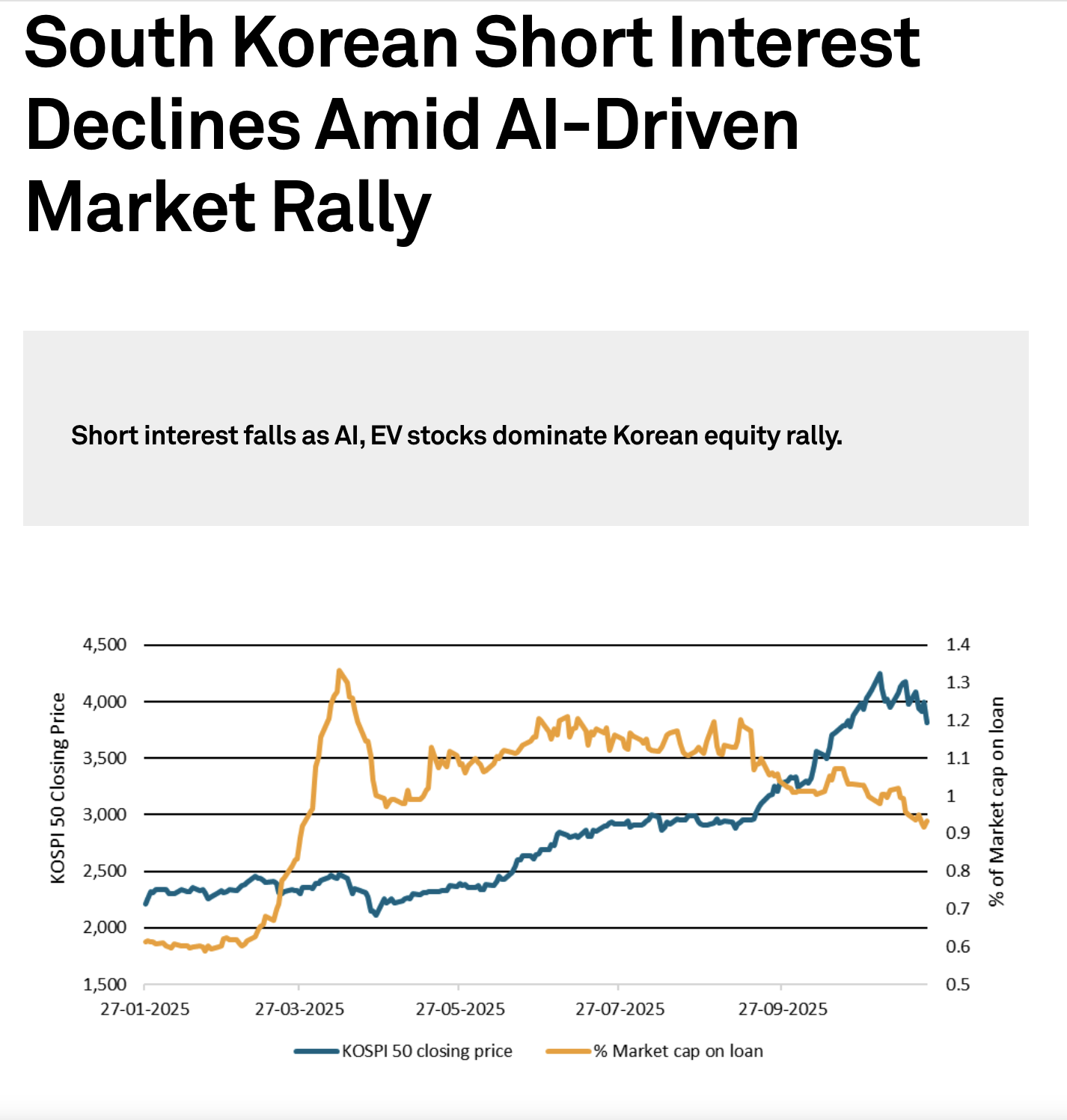

In current real-time conditions, the picture in 2025 closely matches the transmission channels modeled in this project. South Korean equities have staged a strong rally, with the KOSPI up roughly 60% year-to-date and recently trading above the 4,000 level as foreign investors return on the back of AI-driven demand for Korean chip and tech stocks (S&P Global, 2025)1,.

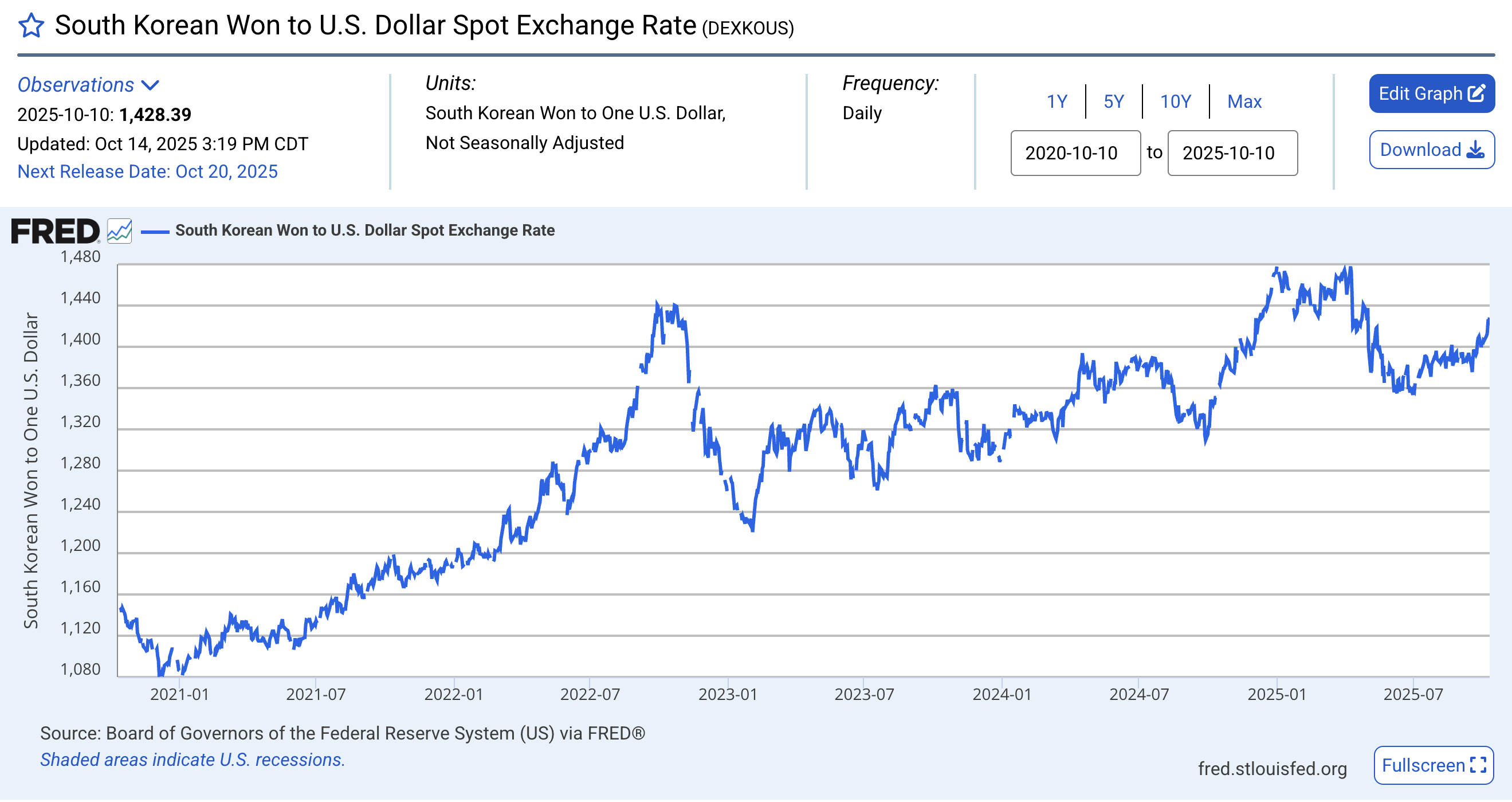

The won, meanwhile, has weakened into the high-1,400s per U.S. dollar in late November and early December, reflecting persistent interest-rate differentials with the United States and sustained demand for dollar assets (TradingEconomics, 2025)2. Parallel exchange-rate data confirm that the won has remained under pressure as global investors favor dollar-denominated assets (ExchangeRates.org.uk, 2025)3 .

The Bank of Korea has kept its base rate at 2.50% while headline inflation hovers around 2.4%, slightly above its 2% target, which limits the central bank’s room to cut rates even as growth concerns and household-debt pressures remain elevated (Reuters, 2025a)4. Other coverage highlights that policymakers are attempting to balance disinflation progress against lingering financial stability risks (Bloomberg, 2025)5. There is also explicit concern that further easing could deepen pressure on the won and amplify imported inflation (Reuters, 2025b)6.

On the trade and policy side, the new U.S.–Korea Strategic Trade and Investment Deal caps most U.S. tariffs on Korean goods at 15%, lowers auto tariffs(Federal Register, 2025)7. Policy and tax analyses stress that these changes are likely to support Korean exporters but also bind Korea more tightly into U.S.-centered supply chains and security frameworks. Official U.S. communications frame the agreement as a way to deepen strategic economic cooperation while promoting resilient supply chains between the two countries (U.S. Department of Commerce, 2025)8. Together, these developments—surging but volatile equity prices, a softer currency, a cautious monetary stance, and new tariff rules—show that shifts in U.S. financial and policy conditions continue to transmit quickly into Korean markets, affecting the value of household savings, the cost of borrowing for firms, and job security in export-oriented industries.