TF-IDF Keyword Analysis

Overview

This page presents the Term Frequency–Inverse Document Frequency (TF-IDF) analysis of 4,791 consumer complaint narratives. The analysis identifies which words best distinguish complaints and compares the keyword profiles of resolved versus unresolved complaints.

Method

TF-IDF vectorization assigns each word a score based on:

- How often it appears in a single complaint (term frequency)

- How rare it is across the entire corpus (inverse document frequency)

Words with high TF-IDF scores are those that are distinctive to particular complaints rather than common throughout. This helps surface the specific harms consumers describe.

Preprocessing steps:

- Lowercase conversion

- Removal of stopwords (standard English stopword list)

- Removal of digits and non-alphabetic tokens

- Minimum document frequency of 5

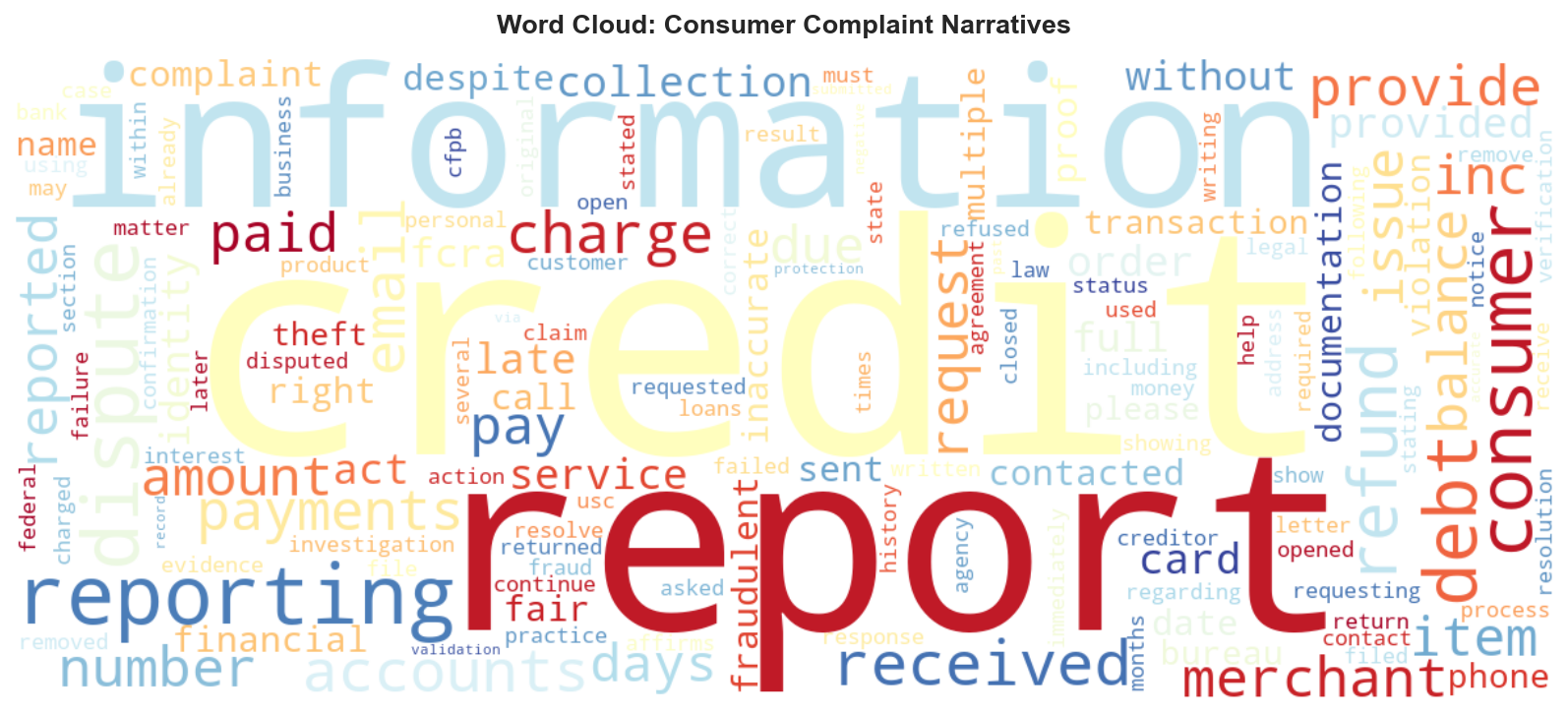

Overall Corpus Word Cloud

The dominant terms — “credit,” “report,” “debt,” “dispute,” “refund” — confirm the findings from the exploratory analysis: BNPL consumers are not primarily describing product dissatisfaction but legal and financial harm.

The prevalence of “dispute” and “report” as core lexical anchors is particularly significant, as these are precisely the mechanisms — dispute resolution and credit reporting — that TILA governs for credit card users but does not mandate for BNPL.

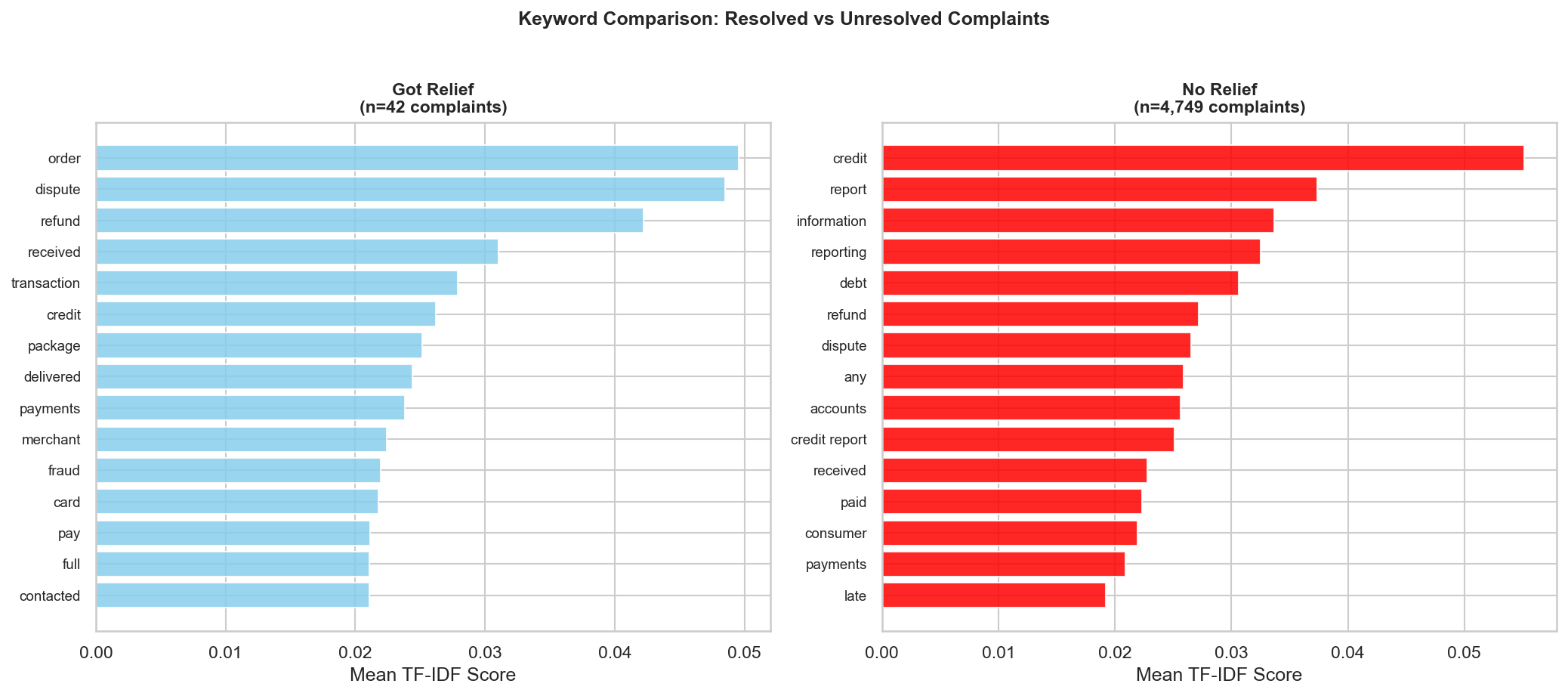

Resolved vs. Unresolved Complaints

Comparing keyword profiles between complaints that received relief (n=95) and those that did not (n=4,696) reveals a stark structural pattern.

Resolved (n=95)

Complaints that resulted in relief are characterized by:

orderdisputerefundtransactiondeliveredpackage

These describe discrete transactional disputes — individual purchases where a merchant-level issue can be resolved internally by the company.

Unresolved (n=4,696)

Complaints that received no relief are dominated by:

creditreportinformationdebtaccountscredit report

These describe systemic credit reporting errors — problems that require correction by credit bureaus, not merely the BNPL company.

Interpretation

This divergence reveals the structural limits of the current complaint resolution framework. Companies can occasionally resolve discrete transactional disputes because the remedy is within their direct control: refund the consumer, reverse the charge, resolve the delivery problem. They cannot — and are not legally required to — correct systemic credit reporting errors that propagate across bureaus.

The complaints that receive no relief are precisely those that a TILA-mandated dispute resolution mechanism would address. Under the Fair Credit Billing Act, credit card issuers are legally obligated to investigate disputes within a defined timeline. BNPL providers face no equivalent requirement.