Regulatory Term Frequency

Overview

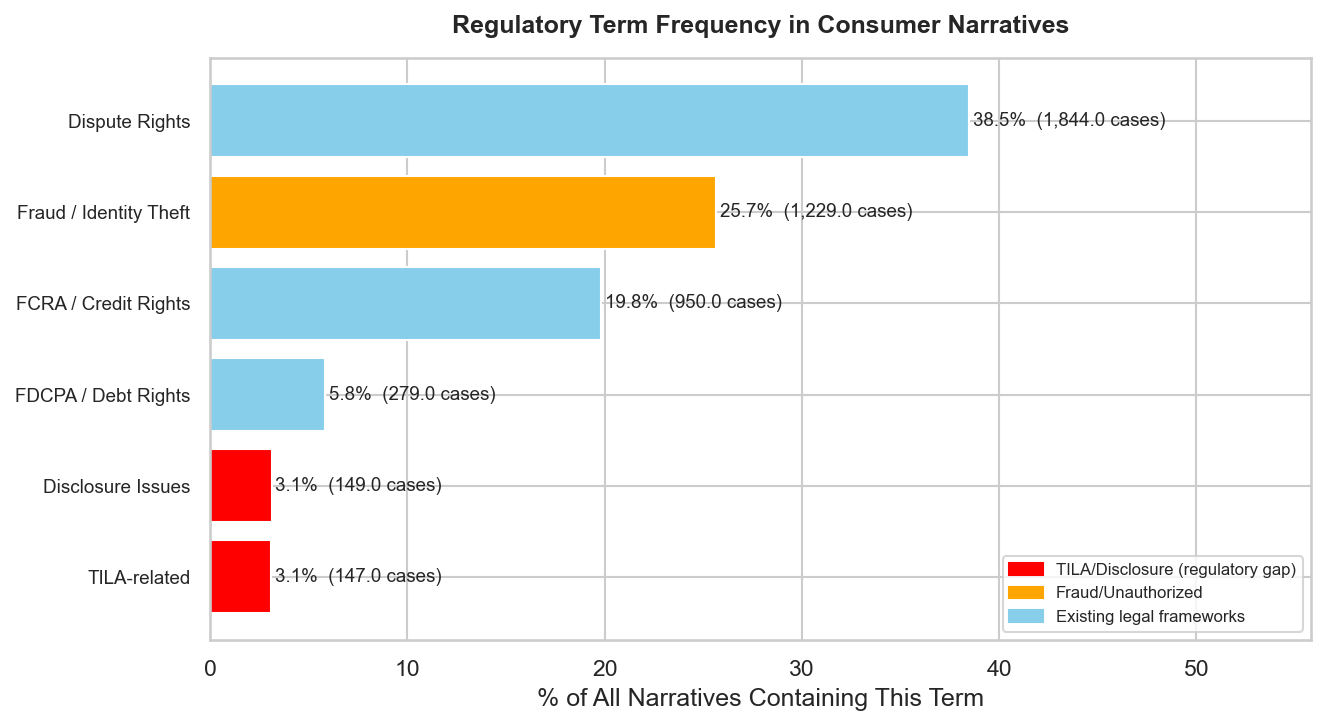

This page quantifies how often consumers invoke specific regulatory concepts in their complaint narratives. The analysis maps consumer language onto existing legal frameworks to reveal which rights consumers know they have — and which they do not.

Method

Each narrative (n=4,791) was scanned for terms associated with five regulatory concept categories:

| Category | Example Terms |

|---|---|

| Dispute Rights | dispute, challenge, investigation |

| Fraud / Identity Theft | fraud, identity theft, unauthorized |

| FCRA / Credit Rights | FCRA, credit bureau, credit reporting |

| FDCPA / Debt Rights | FDCPA, debt collection, validation |

| TILA-related (Disclosure) | APR, finance charge, annual percentage rate |

Each narrative was counted once per category if any of that category’s terms appeared.

Findings

| Regulatory Concept | Cases | % of Narratives |

|---|---|---|

| Dispute Rights | 1,844 | 38.5% |

| Fraud / Identity Theft | 1,229 | 25.7% |

| FCRA / Credit Rights | 950 | 19.8% |

| FDCPA / Debt Rights | 279 | 5.8% |

| Disclosure Issues | 149 | 3.1% |

| TILA-related | 147 | 3.1% |

Silence Is Not Satisfaction

The low invocation rate of TILA-related terms (3.1%) could be misread as evidence that consumers are satisfied with BNPL disclosures. The opposite interpretation is more consistent with the evidence.

Consumers know they have rights under the FCRA because credit reporting disputes are established legal terrain, with decades of case law, consumer-facing educational materials, and a widely understood mechanism for submitting disputes to credit bureaus. They do not invoke TILA because, for BNPL products, TILA does not apply. Consumers cannot assert rights they do not have.

The low frequency of TILA-related terms is not evidence of consumer satisfaction with BNPL disclosures; it is evidence that the legal framework for asserting those rights does not exist.

The Asymmetry of Legal Literacy

The data reveal a form of asymmetry worth making explicit. Consumers routinely use the vocabulary of rights they have:

- “Dispute” (38.5%) — FCBA and FCRA territory

- “FCRA” and “credit bureau” (19.8%) — established federal law

- “Fraud” and “identity theft” (25.7%) — protected under multiple federal statutes

They do not use the vocabulary of rights they lack for BNPL, even though those same concepts would apply to the same transactions if they had been made on a credit card:

- “APR” (part of the 3.1%)

- “Finance charge” (part of the 3.1%)

- “Annual percentage rate” (part of the 3.1%)

This is not a linguistic coincidence. It is the empirical footprint of a regulatory gap.